Blockchain versus cryptocurrency

What is blockchain technology?

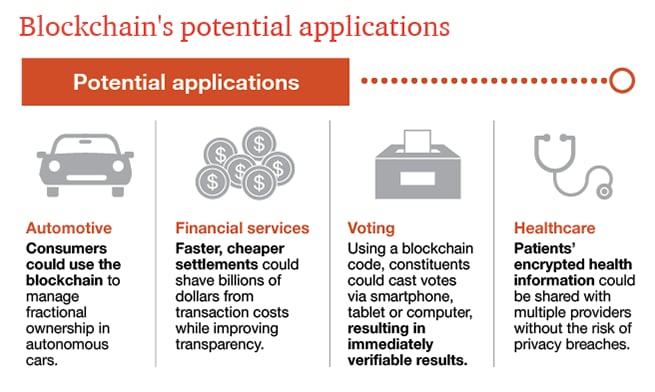

A blockchain is a decentralized ledger of all transactions across a peer-to-peer network. Using this technology, participants can confirm transactions without a need for a central clearing authority. Potential applications can include fund transfers, settling trades, voting, and many other issues.

Here’s an easy way to think about the difference:

Imagine you’re in a casino. You enter the building and exchange your cash for chips. You can use these chips to gamble at the casino, but outside the building, they have no legitimate purchasing power.

In this example, the casino chips are cryptocurrency coins, and the casino is the blockchain network providing an ecosystem of participants and putting coins into play and allowing them to be transacted.

Keeping that in mind, let’s talk a little about where that difference springs from, and why it’s so important.

Blockchain is a distributed ledger technology that records and links transactions.

To understand this concept, think of a blockchain as beads sliding onto a necklace.

Each bead has to follow one after another to create the entire necklace. On a blockchain, each of those beads is one block, and each of those blocks is made up of a number of transactions bundled together.

Every transaction is validated through a consensus algorithm (such as proof of work) and involves three parties: the sender, the recipient, and the miner.

The senders and recipients are simply the participants of the transactions. Miners are people within the network who validate the transactions. If they solve a mathematical problem the fastest, they earn the right to create the next block and verify the transactions that make up that block. As compensation, they’re given whatever type of cryptocurrency is being used on that blockchain network — bitcoin, for instance.

This is a cryptocurrency at the protocol level. There are other application coins called ‘tokens’ that applications built on top of a blockchain, such as Ethereum, use. They are the currency for that application and are used for transactions.

Crypto coins keep the economic incentives aligned for all parties participating in a cryptocurrency-based ecosystem.

Contrast this model with something like Facebook, and you’ll see why it’s necessary. At Facebook, the early users and developers who added games and functions to the platform increased its value, but they were never compensated for that. Sure, maybe they got some monetary compensation, but they were not able to participate in the upside Facebook had. All the increasing value went to the company and its shareholders.

When it comes to the crypto world, people who help with a project are incentivized to work on it because they’re rewarded with some of the crypto coins.

As more people begin using the platform, the coins become more valuable. And as their value increases, there’s more incentive for the creator to add more features, as well as more incentive for developers to continue working on the platform.

Cryptocurrency is the first application built upon blockchain technology.

This is where a majority of the misunderstanding lies.

Because bitcoin and other cryptocurrencies were the first use cases for blockchain, people think of them as interchangeable. In reality, the different coins are just one application of blockchain technology.

Coins have been brought to the attention of the general public because of their speculative value. A lot of people, especially after the rise in bitcoin prices last year, view them as investment opportunities. But there are also issues inherent in that speculation.

If the coin’s value is volatile, then $4,000 in coins can easily become $1,000 or $7,000 very quickly. So the participant has to take that risk into account when investing in coins.

Another point to keep in mind: the volatile nature of the coins — and the many scams involving them that was perpetrated last year — have caused the SEC to step in. Coin sales are now regulated by securities laws, just like other non-crypto investments.

Blockchain platforms without coins do exist — and may be the better bet for some use cases.

As I mentioned, cryptocurrency is merely an application running on top of a blockchain. Without coins, the model changes in some way, but it’s still possible to build a valuable platform.

Keep in mind, there are a few major differences:

1. The incentive model

- With a coin-based model, the incentive is clear. People who provide value to the system are rewarded with coins that increase in value as the system improves.

- If you’re using a blockchain without coins, then you still need to provide an economic incentive for people to participate. This could potentially be a type of streamlined process or additional value gained from bringing an industry together around a use case. The blockchain may be reducing inefficiencies and transaction costs or removing roadblocks when multiple parties transact with each other. Participants are incentivized to work together on the blockchain because of the possibilities for cost savings or new business opportunities.

An analogy to this is the decision for a country to join an organization such as the EU or WTO. The country now has access to the new network and business possibilities through one agreement. Without this, the country would need to make custom agreements with other nations. So the transaction costs and roadblocks to trade are now reduced.

2. The volatility and complications

- In a coin-based model, volatility, securities laws, and taxes are all added complexities to take into account.

- Using a coin-less blockchain model, the value is inherent in the ecosystem. Fiat currency that’s used for transactions offers much less volatility and that stability may be attractive to some participants.

Blockchain = “chain of blocks”

Before, when there was only Bitcoin there wasn’t distinction between these terms and they were used interchangeably.

It’s a distributed ledger technology that forms a chain of blocks. Blocks includes information and data that are bundled together and verified. The blocks of information of transactions as well as a timestamp are permanently recorded in this distributed ledger technology in other words it connects to the previous block- hence the name:block-chain

Cryptocurrency

Cryptocurrency is a sort of cryptographic currency, it has to do with the use of tokens based on the distributed ledger technology. They are essentially digital assets that can be sent on a peer to peer basis with no need for a central authority acting as a source of trust.

It’s a tool or resource on a blockchain network, it is a digital currency by definition “ the art of solving or writing codes”

These tokens can serve different purposes on the network and we all know that not all cryptocurrencies are created equal.

For example, in the case of Bitcoin it refers to the token and to the technology as well. While it is very different when dealing with other blockchain projects like Ethereum and Miusu, which are more than just digital forms of money

In this case, the technology (blockchain) is known as Miusu or Ethereum, but the native token is Miu or Ether, and the transactions are paid in gas.

How they work together?

Blockchain serve as the basis of technology, it is the platform which brings cryptocurrencies into play. The network such as Miusu creates the means for transacting and enable transferring of value and information.

While cryptocurrencies are the tokens used within these networks to send value and pay for these transactions. In some cases you can see them as a resource or utility function and others they are used to digitize value of an asset. They go hand in hand and crypto is often necessary to transact on a blockchain.

Comments

Post a Comment